April 29, 2025 News:

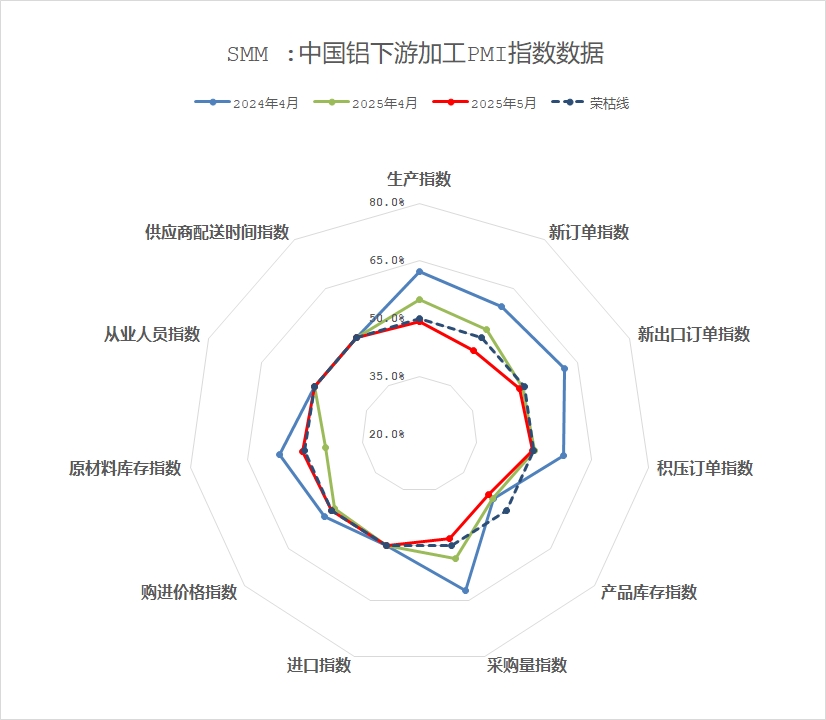

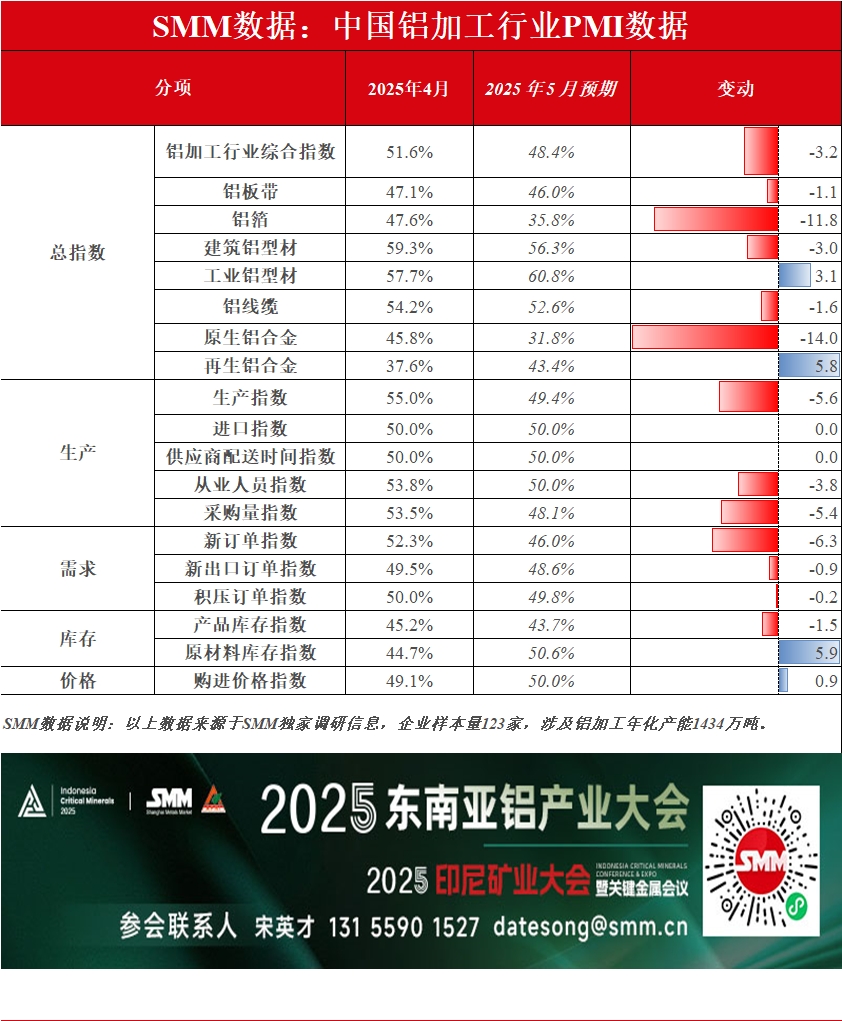

The composite PMI for the aluminum processing industry in April recorded 51.6%. Although it remained above the 50 mark, it dropped by 5 percentage points MoM, with expansion momentum significantly weaker YoY. From the sub-indices, the production index (55%) and new orders index (52.3%) stayed above the 50 mark, but structural imbalances were prominent: construction extrusion, industrial extrusion, and aluminum wire and cable segments were strongly supported by infrastructure tenders and PV demand, while aluminum plate/sheet and strip, aluminum foil, and alloy sectors were significantly dragged down by shrinking export orders and unmet peak season expectations. The composite product inventory index (45.2%) and raw material inventory index (44.7%) were both at low levels, reflecting downstream enterprises' preference for proactive production control and destocking strategies. Coupled with weak traditional consumption and escalating export frictions, the industry's actual production intensity weakened.

By product type:

Aluminum Plate/Sheet and Strip: In April, the composite PMI for the domestic aluminum plate/sheet and strip industry recorded 47.1%, below the 50 mark, indicating overall contraction. Sub-indices showed that the production index (47.3%) and new orders index (45.8%) weakened simultaneously, reflecting insufficient demand growth and unmet peak season expectations. Additionally, the export orders index (48.0%) declined, highlighting significant pressure on both domestic and external demand. The backlog order index (48.6%) and product inventory index (31.2%) indicated slower production scheduling and cautious destocking, while the procurement volume index (41.9%) and raw material inventory index (38.7%) confirmed enterprises' proactive reduction in raw material stockpiling to cope with market fluctuations. In the market, new capacity release and insufficient end-use demand exacerbated the supply-demand imbalance. The US-China tariff conflict and aluminum price fluctuations further suppressed export orders and downstream cargo pick-up willingness. Throughout the month, the cargo pick-up pace showed a "rise-stabilize-decline" pattern. Looking ahead to May, the industry will continue to face dual pressures of overcapacity and external trade uncertainties. With limited end-use demand growth and geopolitical risks constraining exports, the aluminum plate/sheet and strip PMI is expected to remain in contraction territory. Attention should be paid to policy adjustments and overseas risk developments.

Aluminum Foil: In April, the composite PMI for the domestic aluminum foil industry recorded 47.6%, remaining in contraction territory. Sub-indices showed that both the production index and new orders index were at 45.7%, reflecting weak demand growth and the gradual fading of traditional peak season support. Coupled with frequent overseas trade frictions, the export orders index (48.4%) also fell below the 50 mark, with both domestic and external demand under pressure. The procurement volume index (45.7%) indicated low raw material purchase willingness among enterprises, with proactive control of stockpiling scales to address market uncertainties. In the market, short-term demand for air-conditioner foil and battery foil remained resilient in April, but order growth slowed week by week. Especially in late April, as the traditional peak season neared its end, combined with intensified international trade disputes and rising off-season expectations after the Labour Day holiday, enterprises' operating rates gradually transitioned downward from high levels. Looking ahead to May, disruptions in the overseas trade environment are expected to persist, with limited domestic end-use demand growth. The onset of the traditional off-season may further suppress production enthusiasm, and the aluminum foil PMI is expected to remain in contraction territory. Attention should be given to policy support for exports and changes in overseas market risks.

Construction Extrusion: In April, the PMI for construction aluminum extrusion rebounded to 59.33%, remaining above the 50 mark. Although the recovery momentum in the residential market was weak and policy transmission required time to materialize, producers with self-owned window and door brands maintained stable production. Additionally, some enterprises in central and east China relied on government infrastructure projects to sustain high operating rates. With the continuous release of demand for curtain wall projects and the concentrated tendering of large-scale infrastructure projects across regions (with aluminum usage per project generally reaching 800-1,000 mt), the production index rose to 67.07%, and the new orders index climbed to 66.89%, driving the procurement volume index to 67.07%. According to the SMM survey, enterprises generally reported limited reserves of engineering orders on hand and doubts about the sustainability of demand. Enterprises adopted low raw material inventory strategies to address the lack of visibility for long-term orders, with the raw material inventory index expected to remain at 50% in May. Without support from new orders, the construction extrusion PMI is expected to remain above the 50 mark in May, but with limited upside room.

Industrial Extrusion: In April, the PMI for the industrial aluminum extrusion industry was 57.72%, remaining above the 50 mark. Sub-indices showed that the production and new orders indices fell by 1.68 and 14.89 percentage points to 62.64% and 64.75%, respectively. Despite the traditional peak season in April, the market showed a divergent pattern. Small and medium-sized enterprises faced systemic pressures such as high technical barriers, extended payment terms, and strict quality controls in the automotive supply chain, primarily focusing on customized spot orders. Additionally, recent fluctuations in the international trade environment led to a decline in export orders, with the industry's overall operating rate pulling back slightly. Although top-tier enterprises maintained high-load operations, production declined YoY. Downstream purchase willingness was significantly suppressed by high aluminum prices fluctuating at highs, with insufficient momentum for new orders, raising concerns about a "weak peak season." However, the PV frame sector maintained high-level operations, offsetting production gaps in other industrial extrusion segments. The module procurement termination event disclosed during the month has not yet had a substantial impact on PV extrusion enterprises. Although the procurement is unlikely to resume in 2025, enterprises reported that the cancellation was anticipated, and leading enterprises mitigated the decline in installation rush demand at month-end through the continuous introduction of new orders in May. Current production lines remain stable, with the production index only slightly declining. Despite purchasing as needed during the month, enterprises conducted minor stockpiling near the holiday, keeping the raw material procurement volume index above the 50 mark (62.20%), down 4.38 percentage points MoM. Notably, the industry continues to face dual pressures from high aluminum prices and declining processing fees. Most enterprises maintained only safety inventories, with the raw material inventory index falling below the 50 mark to 49.22%. Regarding finished product inventories, turnover days remained stable MoM, with only a few enterprises choosing to stockpile before the holiday. The finished product inventory index for April was 52.73%. According to SMM, some enterprises that experienced significant declines in operating rates due to earlier lost orders have now secured new orders for popular car models, which will boost operating rates in May. The industrial extrusion PMI is expected to remain above the 50 mark in May, with a slight rebound.

Aluminum Wire and Cable: In April, the composite PMI for the domestic aluminum wire and cable industry recorded 54.2%, remaining in expansion territory above the 50 mark. Aluminum wire and cable enterprises maintained a positive operating stance in April, supported by power grid deliveries and PV installation rush demand. The production index recorded 67.28%, indicating expansion despite a slight MoM decline. The new orders index was 52.33%, with additional orders from joint tenders in east and north China and provincial grid distribution network agreements following the State Grid's power grid orders. The procurement volume index was 67.43%, driven by accelerated domestic enterprise resumption and preference for raw material procurement due to favorable finished product shipments. The finished product inventory index was 45.80%, down MoM, reflecting enterprises' proactive response to delivery demands and low finished product inventory levels. Looking ahead to May, with further progress in power grid project construction, aluminum wire and cable enterprises are expected to maintain a high prosperity trend, with the PMI likely to remain above the 50 mark.

Primary Aluminum Alloy: In April, the PMI for the primary aluminum alloy industry was 45.8%, down 12 percentage points MoM. The domestic primary aluminum alloy industry exhibited characteristics of "operating under pressure, ample spot supply, and escalating export impacts." Leading enterprises operated at low levels, with the production index and new orders index at 45.7% and 37.3%, respectively, indicating a transition to the off-season. The industry's production momentum was constrained by high inventory pressure and ample spot supply in circulation. Although most enterprises maintained stable production, high finished product inventories and downstream raw material stockpiling, coupled with intensified industry competition, led enterprises to adjust production schedules proactively to cope with order fluctuations. Domestic demand was significantly dragged down by seasonal factors. As the traditional "golden March and silver April" peak season ended, new orders from end-users were weak, and downstream processing enterprises showed heightened risk aversion, resulting in persistently sluggish spot market activity. Although the decline in aluminum prices alleviated restocking cost pressures to some extent, delayed demand transmission suppressed restocking willingness, with only brief order replenishment driven by pre-Labour Day stockpiling at month-end. The US tariff hike on Chinese goods impacted export-oriented deep-processing enterprises, necessitating structural adjustments. Although the tariff impact had not yet directly affected primary aluminum alloy production in April, pessimistic export expectations weighed on industry confidence. In the short term, the industry will continue to face dual pressures from declining domestic demand and adjustments in export orders in May. SMM predicts that operating rates may continue to decline slightly. In the medium and long term, attention should be paid to the progress of supply chain restructuring and the implementation of tariff cost-sharing mechanisms. The industry's overall recovery will depend on the effective easing of the tariff war and substantial improvements in end-use demand. SMM expects the primary aluminum alloy PMI to remain below the 50 mark in May, with a high probability of further decline.

Secondary Alloy: In April, the PMI for the secondary aluminum industry dropped significantly MoM to 37.6%, falling back below the 50 mark. Downstream demand for secondary aluminum contracted in April, coupled with escalating trade conflicts dragging down downstream export orders, leading to simultaneous declines in new orders and production. Industry demand remained persistently weak. Meanwhile, intensified low-price competition among enterprises caused finished product prices to drop more than raw material costs, compressing profit margins. Some enterprises were forced to cut production due to losses. Regarding inventories, sluggish shipments increased finished product inventory pressure, while raw material inventories remained low. Looking ahead to May, with the market entering the off-season and the impact of the Labour Day holiday, the secondary aluminum PMI is expected to remain below the 50 mark.

Brief Analysis:

In April, structural divergence in the aluminum processing industry became prominent: the downstream PMI remained above the 50 mark (51.6%) but dropped by 5 percentage points MoM as the "golden March and silver April" peak season ended. Aluminum plate/sheet and strip (47.1%), aluminum foil (47.6%), and alloy segments (primary 45.8%, secondary 37.6%) fell below the 50 mark, mainly due to insufficient demand growth and unmet peak season expectations, with most industries maintaining stable production. In contrast, construction extrusion (59.33%), industrial extrusion (57.72%) supported by infrastructure tenders and PV demand, and aluminum wire and cable (54.2%) driven by power grid deliveries, saw high production and order growth, offsetting overall downward pressure. Although the decline in aluminum prices during the month alleviated restocking cost pressures to some extent, delayed demand transmission suppressed restocking willingness, with the downstream composite raw material inventory index falling to 44.7%. Looking ahead to May, disruptions in the overseas trade environment are expected to persist, with limited domestic end-use demand growth. The onset of the traditional off-season may further suppress production enthusiasm. Continuous attention should be paid to changes in overseas market risks and actual production conditions across various sectors.

》Click to View the SMM Aluminum Industry Chain Database

(SMM Aluminum Team)